What does this mean of investing?

What is the purpose of having money? Is it so that you can put it in a bathtub and roll around in dollar bills (or hundred dollar bills) a la Scrooge McDuck? Money is used to purchase the things and the services that you want. Just as Austrian economist Ludwig von Mises explained in The Theory of Money and Credit, money is a medium to serve instead of barter.

Let’s look at why money serves the purpose it does, and then we can move on in our discussion about how that affects your financial life cycle. Basic economic theory explains that money serves as an intermediary to prevent us from having to barter all the time. Imagine if you were a shoemaker in a world without money. You make shoes which people need to keep their feet from getting injured or to sprint like Hussein Bolt. However, people don’t need new shoes all the time. They only need them occasionally, probably about annually. So, you have to find different people who need new shoes all the time.

So, with much hustling and effort, you’re able to get a steady stream of customers. What do they give you in exchange for your shoes? You need food, someone to help you build your house, clothes, water, security, etc. Therefore, for a barter system to work, you either have to continually match your shoes with people who both need your shoes AND can offer you something you need in return, or you have to centralize demand and supply through an intermediary. In this scenario, an intermediary would get rich because she could demand a pair of shoes, a dozen eggs, wood, and many other things for her services to save you from having to find all of those suppliers who also happened to need shoes yourself.

Instead, we use money. It is, in effect, a delayed exchange of goods and services. You make shoes and when someone buys the shoes, you get money. This money is a promise that you can buy goods and services you need sometime later. Now, you no longer need to go find someone who can supply you with food who concurrently needs shoes. Money eliminates the need for direct trading and for an intermediary.

Back to the present and how the function of money affects your life cycle planning. As we covered before, the purpose of money is to enable you to buy goods and services. There are three main ways to get money (and, no, the lottery does not count as one of the ways to get money):

- Earn money through work. From the time you cut grass as a teenager until you walk out of the office for the last time to go to your retirement party, people pay you for the value you can create. For most people this period of earning capability lasts between 40 and 50 years, and is the time when your human capital provides you with the most economic firepower. The more you can earn, the higher your chances of having enough money to do what you want without running out are. For most people, this is the biggest driver of monetary accumulation. That’s why I encourage people to invest in themselves.

- Earn money through investing. This is what people are trying to achieve through investing in mutual funds, bonds, stocks, CDs, and money markets. It’s also where private equity and angel investing fit. In essence, you are becoming the intermediary for others’ human capital. You indirectly pay someone else to create value and you get a piece of the profits from that value creation. Sometimes it doesn’t work out, and people create less value than expected, and you lose some (or all of) your money. We encourage people to use this means of earning money to meet or beat inflation.

- Receive money through inheritance. Sometimes, you strike it lucky. Rich uncle Willie, who you met once when you were a precocious 2 year old, took a shine to you and left his entire gazillion dollar estate to you. Welcome to the yacht club. Most of the time, you will either not inherit any money, or the money you inherit will not be enough to meaningfully influence your life. Depending on inheritance to secure your financial future is foolhardy and depraved. If you do this, you’re hoping someone else dies so that you can prosper. Sick. Furthermore, all it takes is one stroke of the pen, and that inheritance will go to Fluffy the cat. We encourage people to use inheritance, if received at all, as a windfall to add to ensure progress towards their life’s priorities.

For a vast majority of people, the first category is where they’re going to get a significant portion of their money – from working. They can either work for a boss or for themselves, but they’re going to have to work to earn money.

What about the primary purpose we discussed earlier – spending money?

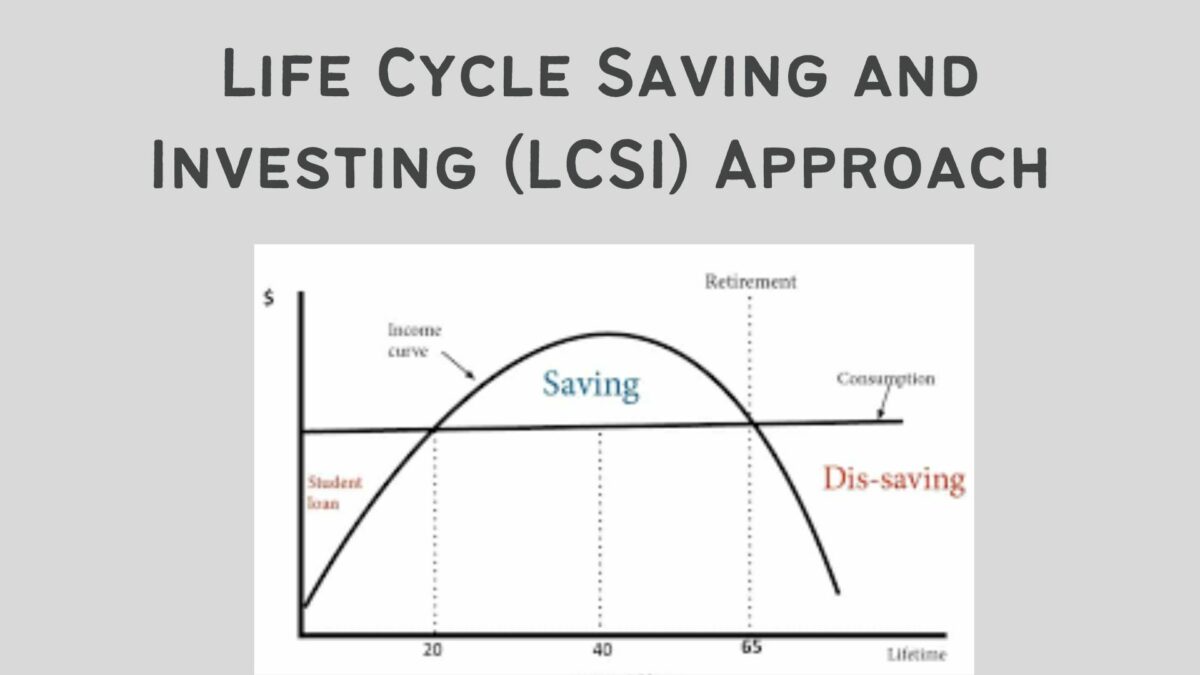

Let’s assume that you work for 40 years, lived with your parents for 20 years (and therefore, had no independent expenses), and live for 80 years. This means that you have 40 years’ worth of earning power to account for 60 years of spending.

If you plot spending over time, it looks like a big hill and then a small hill.

The first hill is from your early 20s to your mid-70s. When you first start out, you probably don’t live very lavishly. If you’re like most 20-somethings with a college degree, you have quite a bit of debt that you have to get out from under. So, you live in a tiny apartment using cardboard boxes and lawn chairs as your furniture. You eat ramen noodles (hey! No different than college, right?), and you buy and wash Styrofoam containers for your dishes.

As you get traction in your job, you start to get paid more. You start to get your student loan balance under control, and you can expand your standard of living some. You meet that Special Someone(TM), and you get married and have 2.2 children. You’ve combined incomes so have more money, but kids are expensive, so your spending also goes up, since kids somehow keep demanding food and can’t make a t-shirt last 18 years. Eventually, the kids move out (hopefully) for good and your expenses start to go down. All during this time, you’ve been getting promotions, finding new jobs, and generally increasing your income to keep up with, and ideally exceed your expenses.

So, when the kids move out, you may find yourself flush with money. It’s like getting a raise! You’re in your 40s or 50s and at the peak of your earning power, and your expenses have suddenly dropped because there aren’t any hungry, growing mouths to feed in the family.

Here’s where a lot of people make a tremendous financial mistake.

They see this sudden gush of money as a reason to increase the standard of living. Dad goes out and gets the convertible Corvette to have the wind blow through his combover and Mom gets the Joan Rivers botox treatment. Life is good! No kids, no responsibility!

Except, of course, they forget about the responsibility to their future selves, the ones who can no longer earn money at work. This is the limbic system, or Monkey Brain, at work. It wants pleasure NOW. It also doesn’t care about the future Monkey Brain, which will also want pleasure.

Finally, the day of the retirement party comes. Once upon a time, there was a golden watch and a pension to see you out for the rest of your days. Nowadays, your chances of receiving a pension are slim. According to a 2004 Bureau of Labor Statistics report 34% of workers participated in a pension plan; that number has likely dropped in the intervening years, as only 11 of the Fortune 100 companies offer pension plans to new workers.

Still, even though you’ve stopped working and probably don’t have a pension, the expenses don’t go away. You still need to buy food and pay for shelter, and you’d probably like to take trips to go see the grandkids. You don’t need to buy work clothes, and you’re not driving to work every day, so your expenses do drop. Expenses should go down the first hill that we discussed earlier. You may have Social Security payments, but that is meant to be a supplement to other sources of money, not a primary source of money.

Then, as you get older, your body starts to break down, unless you’re Jack Lalane. The knees creak and the eyes start to go bad. Your medical expenses will rise, and eventually, you won’t be able to live independently. This begins the second hill – when medical and health costs rise. Even before your lose your independence, your health insurance bill will go up, because even if you’re not in need of extra healthcare services, many people your age are.

So, how do you ensure that you’re not eating cat food when you’re older? That is the purpose of saving – to smooth out your consumption so that you can move money from times of high earning to times of low earning. Banks participate in this transaction all of the time. That’s why you’re able to get student loans to pay for college and a mortgage when you buy your first house. Loans shift future earnings into present consumption when you’re younger. It’s also risky; it depends on you having a higher future earning than you do now. Savings shift higher present earnings into future consumption when you have lower earnings.

If you match your consumption to your earnings, then you’re going to get to relive the days of lawn chair furniture, Styrofoam dishes, cardboard boxes, and ramen noodles when you’re elderly. It’s probably not a vision of the future that you have in mind. That is why maximizing your human capital, saving money, and living below your means (LBYM) is so important. You’re trying to spread out the years of earning money to match the years of spending money. Your consumption won’t be a flat line throughout your life either, but if you don’t live below your means and save and invest money when you’re earning it, your consumption will flatline when you get older.

It’s not a flatline you want.

Author Profile

- John Davis is a nationally recognized expert on credit reporting, credit scoring, and identity theft. He has written four books about his expertise in the field and has been featured extensively in numerous media outlets such as The Wall Street Journal, The Washington Post, CNN, CBS News, CNBC, Fox Business, and many more. With over 20 years of experience helping consumers understand their credit and identity protection rights, John is passionate about empowering people to take control of their finances. He works with financial institutions to develop consumer-friendly policies that promote financial literacy and responsible borrowing habits.

Latest entries

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide Low Income GrantsSeptember 25, 2023Dental Charities That Help With Dental Costs

Low Income GrantsSeptember 25, 2023Dental Charities That Help With Dental Costs Low Income GrantsSeptember 25, 2023Low-Cost Hearing Aids for Seniors: A Comprehensive Guide

Low Income GrantsSeptember 25, 2023Low-Cost Hearing Aids for Seniors: A Comprehensive Guide Low Income GrantsSeptember 25, 2023Second Chance Apartments that Accept Evictions: A Comprehensive Guide

Low Income GrantsSeptember 25, 2023Second Chance Apartments that Accept Evictions: A Comprehensive Guide