This is part of a series. If you have not read the articles that build up to this one, I recommend that you do so first.

- Answering the Question Why About Your Money

- Monkey Brain’s Common Weapons

- Money Comes and Money Goes

- Cracking the Whip on Your Money

- A Contract on Your Life

- What if You Can’t Work (and Not Just From a Lack of Coffee)?

- Don’t Pay an Arm and a Leg to Keep Your Arm And Leg

- Long Term Care Insurance

- Investing Doesn’t Mean Playing the Markets

- How to Save for Retirement

- Retirement – Paying for Knee-High Socks and Hammocks

- How Much Should I Be Saving?

- Social Security – Neither Social nor Secure, But It’s Something

Up until now, we haven’t really talked about anyone outside of a truly nuclear family: you and your spouse. If you have them, you probably included your kids in the article about priorities and you certainly included them in the article about budgeting. You may have thought about them in the retirement planning articles (retirement, saving for retirement, and Social Security planning), depending on whether or not you want to leave them with an inheritance. Now, we’re going to focus specifically on them, how much they cost, and how you can manage your finances with kids in the picture.

One of the great mysteries that you face, besides whether or not your kid will turn out to be a fine, upstanding citizen, or, despite all of your efforts, become a slacker, is just how much a kid is going to cost you if you decide to have one. While the cost of having children almost certainly won’t affect your decision to have them one way or the other, knowing what you’re facing and how your life will change will arm you to make an informed decision.

The United States Department of Agriculture does a pretty comprehensive study on how much families spend on raising children. The results are unsurprising.

- If you make more money, you’ll spend more money on your kids. If you make less money, you’ll spend less on your kids.

- If you’re a single parent, you’ll spend less money on your kids than if you are married.

- Older kids cost more than younger kids.

- How much you spend depends on where you live.

Now that I’ve summarized what you could have figured out with a couple of minutes of thinking or with a phone call to your own parents, let’s look at some of the categories of spending. For most families, regardless of socio-economic status, the categories remained relatively the same. Housing was the largest expense as a proportion of the money spent, with food being next, and then, depending on the affluence of the family, education. Another factor was the number of children that the family has. For families with more than one child, the spending drops by roughly 22% with subsequent children. Some of the costs are fixed; each child has to eat food, go to the doctor, go to school, etc. However, the second kid gets hand-me-downs, kids sometimes sleep in the same bedroom, and so forth. Thus, when you have additional kids beyond the first child, you can get some economies of scale in raising the kids.

The best way to give you an idea of roughly how much money you’ll spend and where that money will go is to show it to you graphically.

The numbers show what average families across the United States are spending on their children. There are obviously some factors which would change the picture. For example, if you already have a large house, then you won’t spend as much in housing. Your utilities may run higher, since you’re having to wash more clothes and dishes and you’re using more water, but you won’t have to go get a different, larger home to accommodate your family. If you live in a rural area as compared to New York City, your costs will be lower. You can check out our research on the relative costs of living and retirement savings based on over 200 locations in the United States to see exactly how where you life affects your expenses and how much you need to save for retirement.

What does tend to remain the same, aside from housing, since that depends on your existing housing situation, is the percentage of income that people spend on their kids. As kids get older, parents spend a higher percentage on the kids. As the number of kids increases, the percentage of income per child changes, although the total amount increases.

To help you understand what costs you will likely face in raising kids, I have developed a spreadsheet based on the data which the USDA provided in the aforementioned study (NOTE: it’s a .zip file format to save on upload/download sizes).

Please note: the USDA did not include families with more than 3 children, since there aren’t that many families with more than 3 kids. This model is designed for family expense estimating for families with 1-4 children.

In this spreadsheet, there are three cells where you need to input information.

Once you have input the information, the spreadsheet will provide you with an estimate of how much you will spend in certain categories based on the age of the kids. The left column shows the total amount per category, and the right column shows the average expense per child for each category.

Since, unless you have twins/triplets/etc., you won’t spend that amount concurrently, you can pick and choose from appropriate ages to get an estimate of the total amount. For example, if the family in the example shown above has a 1 year old and a 5 year old, they can expect to spend $35,148.72 on the kids this year.

There are two costs which the USDA study doesn’t cover that you will need to account for as parents.

The Parenting Wage Gap

The sad fact of life is that mothers share an imbalanced financial burden when it comes to raising children. Mothers earn 73% of what men earn, while, ironically, fathers earn 4% more than men who are not fathers. Between the time off of work, some of which may be unpaid, that one or both parents will face and the subsequent expected overall decrease in earnings, parents need to account for the likelihood that the income projections they had prior to having kids are going to dramatically change.

Additionally, many parents want to become stay-at-home parents. There are certainly tradeoffs to consider when looking at that route. Since childcare/education costs comprise a hefty chunk of the costs of raising a child, the difference between foregoing an income and not paying for childcare and education versus having a second income and paying for childcare and education sometimes isn’t all that drastic.

Furthermore, there are benefits and tradeoffs which simply cannot be quantified or calculated with dollars and cents. It’s impossible to measure the benefit that a child gets from being able to spend that much more time with a parent or with both parents as opposed to daycare, childcare, or a nanny. It goes back to the priorities that we listed out in “Answering the Question Why About Your Money.” If child rearing is truly a priority in your life, then you will need to make other spending decisions take a back seat to the child rearing costs – both expenses and opportunity costs.

As much as the quantitative modeler in me hates to admit it, there is no clear cut answer for how to figure out whether or not having a parent be a stay at home parent is the right one. You need to create a long-term budget. Use the costs that you determined in the spreadsheet described above to determine what you’ll be spending each year. Adjust the mother’s income down by 27% to account for the average wage gap that mothers face in the workforce. Then see what your overall spending situation is, accounting for all of the other non child-related expenses as well, and see how that impacts your other goals, such as retirement.

Remember, when you run those estimates, you should already have a retirement number in mind based on the exercise you previously did for calculating your target amount saved up to retire. You may need to adjust the date of retirement based on the decisions you make regarding how much to spend on your kid(s) and whether or not you want to have a stay at home parent. You may reduce the time that the parent stays at home and foregoes the income.

For most people, this is an exercise in tradeoffs. Unless you have a significantly high income or a significantly strong stockpile of assets, you will not be able to have it all – both parents being full-time parents for the kids and indulging them in everything. Use the spreadsheet and the expectation that incomes will change to help you understand what those tradeoffs are and make informed decisions.

The Three Things to Teach Your Kids to Improve Their Chances of Financial Success

I readily confess that I don’t know what truly makes a successful child. Then again, neither did Dr. Benjamin Spock or any of the hordes of parenting gurus who have written every possible Dummies guide about parenting imaginable.

What I can explain, though, are the three aspects of a child’s life that studies indicate lead to higher financial success as adults. These are not surefire guarantees, and failing to teach your kids these skills won’t necessarily doom them to a live of poverty, but statistics certainly point to a strong linkage between knowing these skills and being financially successful later in life.

The first skill is self-control and delaying gratification. This was demonstrated in a famous experiment where five year old children were placed in a room with a marshmallow. They were told that they could eat the one marshmallow now, or, if they could wait 15 minutes, they could have two marshmallows. The children who were able to wait to eat two marshmallows subsequently had higher SAT scores and better coping abilities; they were less obese and had fewer addictions; and 40 years later, they were better able to resist temptation and delay gratification. All of these point to being more financially successful in life as well.

Subsequent research has shown another key in kids’ ability to exert self-control – the trust that they will actually receive the reward promised. A follow-up experiment showed that children who had seen that the people making them promises were actually able to delay the gratification and take two marshmallows later up to four times as often as kids who didn’t receive those reassurances. Thus, not only do you need to establish the benefits of delaying gratification, but when the kids do delay gratification, you need to ensure that they receive the rewards of the delay.

The second aspect of improving a child’s chances of success is teaching them basic math and reading skills at an early age. A study by the University of Edinburgh tracked 17,000 kids in England, Scotland, and Wales. The study tested the basic math and reading skills of those children at age 7 and then evaluated their socioeconomic status 35 years later, at age 42. Boys who demonstrated strong math skills, and girls who demonstrated both strong math and reading skills had a higher income than those who did not, all other factors notwithstanding. For girls, an increase in one level in reading at age 7 translated into an average salary increase of $7,750 per year at age 42.

A third skill to teach your children is the value of hard work. A Stanford study showed that when you praise a child’s hard work and effort rather than his intelligence when faced with a challenge, you are encouraging the child not to give up when he comes upon a difficult situation. When your child accomplishes a task, praise the process (you worked really hard) or the outcome (this room is really clean) rather than the person (you’re a great kid). This is particularly important for elementary school aged girls, as personal praise is counterproductive. Thus, if you get a bumper sticker that says “I’m the parent of a great kid at Smith Elementary School,” don’t put it on your car. Your kid doesn’t go to Smith Elementary anyway!

Remember, none of this is guaranteed; however, the studies show strong correlational evidence of the impacts possessing those skills have on the children when they become adults.

College Saving and Investing

The major cost that the USDA study, and, hence, the worksheet described above does not cover is the cost of college education. While studies have shown that there is an increase in GPA for college students who do not have their education paid for by their parents, many of you will have a very tough time taking that firm of a stand on whether or not you’ll help put your kid(s) through school.

For those of you who decide that you’re going to help the kids out, then there are several ways to accomplish the goal of putting the young ‘uns through college without leaving them saddled with the anchor of an enormous student loan balance when they graduate.

If you haven’t already done so, I recommend you look at my Ultimate Guide to College Education before moving on. I will assume throughout the rest of this article that you have already done so.

I have a simple rule for determining whether or not to fund a Coverdell Education Savings Account versus a 529 plan.

If you’re paying for private schooling before college, use an ESA. Otherwise, use a 529 plan.

Pretty simple, huh? You may also contribute to both an ESA (for pre-college funding) and a 529 plan (for college funding). ESAs are not prohibited for use in college, but only Coverdell ESAs can be used for private schooling payments. There are also greater restrictions on ESAs than there are 529 plans, namely in transferability.

The biggest question that you must attempt to answer before deciding whether or not to invest money into one of these tax advantaged programs for your child is whether or not you think your child is going to go to college and if you want to help pay for it. The biggest deterrent in these programs is that if your child does not go to college and you need to withdraw the money for other reasons; if the money is not used for educational expenses (or one of the limited exceptions), there is a 10% penalty on the earnings. You won’t lose your money, but you will pay a pretty hefty fine.

Still, the tax advantages of the programs make them worthwhile if you think there’s a chance that your kids or other family members will go to college and you want to help them out.

Thus, the biggest question remaining, once you decide to fund a tax advantaged educational account, is how much to save for your kid’s college education.

Inflation for college tuition has been higher than overall inflation, at 4.8% compared to roughly 3% for all other spending. This means that college costs will be more year over year than milk, gas, or other typical consumer staples, and you’ll probably have to save more in order to be able to pay for school.

There is a worksheet associated with this article titled “College Savings Worksheet” (or the macro-enabled College Savings Worksheet (NOTE: it’s a .zip file format to save on upload/download sizes) which can help you figure out how much you’ll need to save or how much you’ll need to either receive in grants and scholarships or ask your child to take on in paying for college costs.

Since costs differ based on state, this worksheet lists out average in-state tuition costs plus room and board for public schools in each state. It also shows the average inflation rate for that particular state’s tuition.

When you open up the spreadsheet, the first thing to do is pick the state where the school is.

Once you pick a state, the average tuition/room and board and inflation rates will automatically fill in.

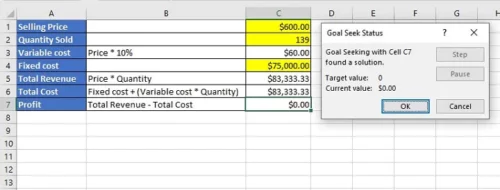

Next, you will need to enter in the number of years remaining until your child starts college, the amount you have already saved for college, and your expected rate of return on your investments. A conservative rate of return would be 5%.

Finally, you will need to enter in your annual contribution. After entering in your annual contribution, the worksheet will return two numbers: an estimate of how much will be in the college savings by the time your child starts school, and the shortfall in paying for four years of college.

At this point, you can use Excel’s Goal Seek functionality to solve how much you need to save annually to leave zero balance. I have automated the function for you, so all you need to do is hit CTRL-SHIFT-K after you change any cell’s information, and it will solve for you.

Do not worry if the cell shows (0.00). That’s the same as zero.

You may also manually enter in different information in cells B2 and B3; however, make sure you do not save the sheet, as these are formulae rather than numbers. If you change the numbers and want to go back to the formulae, simply hit Undo until the formula returns. The College Board has great information about the costs of private and public schools.

If you try to run the spreadsheet and you get a warning about macros running, follow the directions here.

Now that we’ve seen about raising, feeding, and educating our kids, we’ll address another common topic – how to find the right place to live – in a future article. You can also see how where you decide to live affects how much you need to save to retire.

[1] Ibid.

[2]http://www.jstor.org/discover/10.2307/2646943uid=3739920&uid=2&uid=4&uid=3739256&sid=21102000 023333

[3] https://www.mitpressjournals.org/doi/abs/10.1162/003465302317411514?journalCode=rest

[5] http://www.sciencedaily.com/releases/2011/08/110831160220.htm

[6] http://www.webcitation.org/62C1bpSDU

[7] http://www.eurekalert.org/pub_releases/2012-10/uor-tms101012.php

[9] http://academic.reed.edu/motivation/docs/Corpus_Lepper_07.pdf

[10] http://www.cashmoneylife.com/dont-pay-for-your-kids-college/

[11] http://trends.collegeboard.org/sites/default/files/college-pricing-2012-source-data_012413.xlsx

[12] http://trends.collegeboard.org/sites/default/files/college-pricing-2012-full-report_0.pdf

Author Profile

- John Davis is a nationally recognized expert on credit reporting, credit scoring, and identity theft. He has written four books about his expertise in the field and has been featured extensively in numerous media outlets such as The Wall Street Journal, The Washington Post, CNN, CBS News, CNBC, Fox Business, and many more. With over 20 years of experience helping consumers understand their credit and identity protection rights, John is passionate about empowering people to take control of their finances. He works with financial institutions to develop consumer-friendly policies that promote financial literacy and responsible borrowing habits.

Latest entries

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide Low Income GrantsSeptember 25, 2023Dental Charities That Help With Dental Costs

Low Income GrantsSeptember 25, 2023Dental Charities That Help With Dental Costs Low Income GrantsSeptember 25, 2023Low-Cost Hearing Aids for Seniors: A Comprehensive Guide

Low Income GrantsSeptember 25, 2023Low-Cost Hearing Aids for Seniors: A Comprehensive Guide Low Income GrantsSeptember 25, 2023Second Chance Apartments that Accept Evictions: A Comprehensive Guide

Low Income GrantsSeptember 25, 2023Second Chance Apartments that Accept Evictions: A Comprehensive Guide